Introduction to Electronic Payment System

An electronic payment system (e-payment system) is a technique of making transactions or paying for products and services without using checks or currency. The electronic payment system has evolved in recent decades due to the increased popularity of internet-based banking and commerce. As the world evolves technologically, we can grow in electronic payment systems and payment processing equipment. As the percentage of transactions using checks and cash decreases, they grow, develop, and provide more secure online payment transactions ever.

"Nothing is handier than electronic payment when it comes to payment alternatives. You won't have to write a check or deal with any cash. Type some information into your Web browser and click your mouse. It's no surprise that electronic payment, often known as e-payment, is becoming more popular as a substitute for mailing checks through the mail".

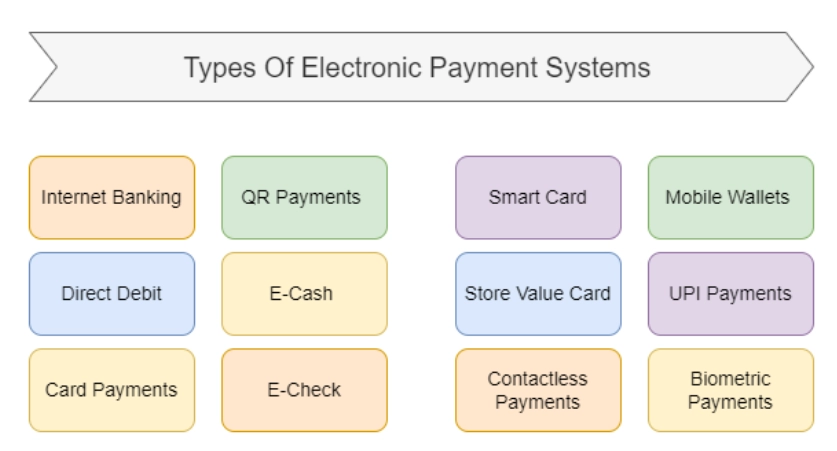

Types of Electronic Payment Systems

-

Internet banking - In this situation, the payment is made by digitally transferring funds from one bank account to another over the internet. NEFT, RTGS, and IMPS are the most common net banking methods.

-

Card Payments - They are made through cards such as credit cards, debit cards, smart cards, stored value cards, and so on. An electronic payment acceptance device begins a card-based online payment transfer in this method. Credit/Debit Card — An e-payment technique that requires the use of a card to make payments using an electronic device.

-

Smart Card - A smart card, sometimes known as a chip card, is a card with a microprocessor chip used to transmit money.

-

Stored value card — These cards have a pre-loaded amount of money and are required for cash transfers. Ex - Gift Cards.

-

Direct debit - With the aid of a third party, direct debit transfers payments from a customer's account.

-

E-cash — This is a method of storing money on a customer's device, then used to make transfers.

-

E-check — An electronic counterpart of a paper check that may be used to transfer payments between accounts.

-

E-wallet: It is a type of electronic wallet. An E-wallet is a prepaid account where clients' account information, such as credit/debit card information, is saved, allowing for a rapid, seamless, and smooth transaction flow.

-

Mobile wallet — A more advanced version of an e-wallet, mobile wallet is widely utilized by many clients. It's a virtual wallet that lives on a mobile device in the form of an app. On a mobile device, a mobile wallet contains card information. Mobile wallets are easy to use since they are user-friendly. It provides a frictionless payment experience, reducing customers' reliance on cash.

-

UPI payments - UPI is the name of the payment system (Unified Payment Interface). UPI payments are done using a smartphone app. NPCI (National Payment Corporation of India) has created an immediate real-time payment system to ease interbank transactions.

-

Biometric payments - Biometric payments are made by scanning/using various body portions, such as fingerprints, eyes, and face recognition, among others. These payments eliminate the need to input a PIN while completing a transaction, making them more accessible and convenient to use.

- Contactless payments - For quite some time, contactless payments have gained popularity. RFID and NFC technologies are used to make these payments. The customer needs to tap or hover the payment device or a card near the payment terminal, earning it a name, 'tap and go.'

32+ registered

32+ registered